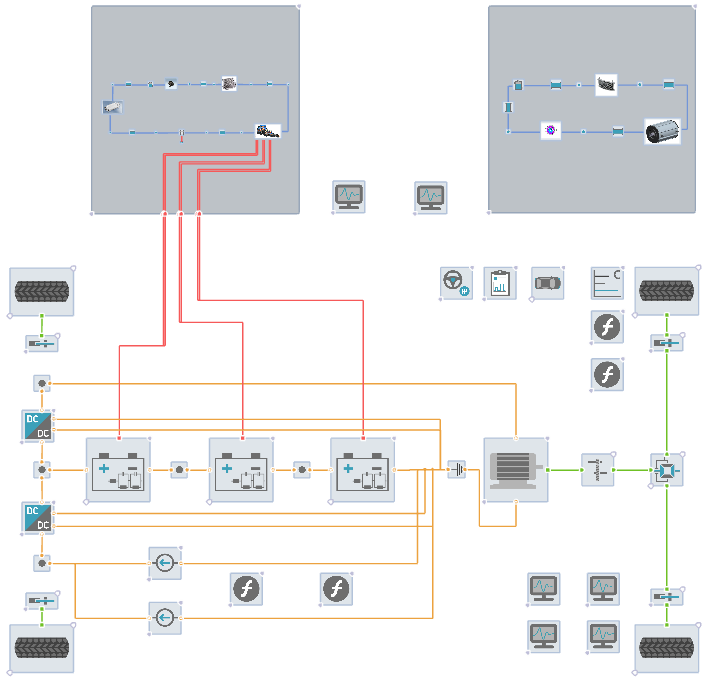

Significant Simulation Time Reduction by the Multi-rate Approach in CRUISE™ M

The

simulation of typical CRUISE™ M applications as for instance hybrid,

battery and fuel cell electric vehicle models requires the coupling of

electric, mechanical, fluid and thermal networks. Each network is

established by combining the physical equations and connection structure

of elementary components and results in a differential algebraic

equation (DAE). In order to speed up the simulation, a non-iterative

multi-rate time integration co-simulation method for the system of

coupled DAEs has been developed and released in CRUISE™ M 2019 R2.

credits: AVL

MathConsult has been doing cooperative research in automotive simulation together with AVL since 2002.

Michael Liebrecht presented our results on the modelling and simulation of leveling machines at NUMIFORM 2019 in Portsmouth, New Hampshire (see the abstract below). These were obtained jointly with voestalpine Grobblech.

Process Model for the Industrial Plate Leveling Operation with Special Emphasis on Online Control

M. Liebrecht, A.-K. Baum, R. Wahl, M. Aichinger, and E. Parteder

To produce high quality steel plates that meet the customer’s requirements, physically based models are increasingly used in the automation systems of the production process. In this work, a 2D model to describe the levelling process of the heavy plate production is presented. The model is based on Euler beam theory and features isotropic hardening of the material and the elastic response of the leveling machine. It enables the computation of the full stress-strain-history, all contact points and contact forces between the plate and the levelling rolls as well as the power consumption. The results are validated using the multi-purpose finite element software ABAQUS and compared to measured forces recorded during production. Core of the implementation is a damped Quasi-Newton method to minimize the free enthalpy of the system. Changes of the mechanical properties of the plate caused by the levelling operation can be calculated from the stress-strain history.

The computation time of the presented full 2D model is dramatically lower compared to the multi-purpose finite element solution. Nevertheless, due to time constraints during the production process, it is not feasible to apply the full 2D model in order to determine the optimal positions of each levelling roll before plates enter the leveler. To achieve this goal, a surrogate model based on vast parameter studies was developed. The parameter studies were performed using the full 2D model and cover all possible levelling roll positions and a wide range of material behaviour.

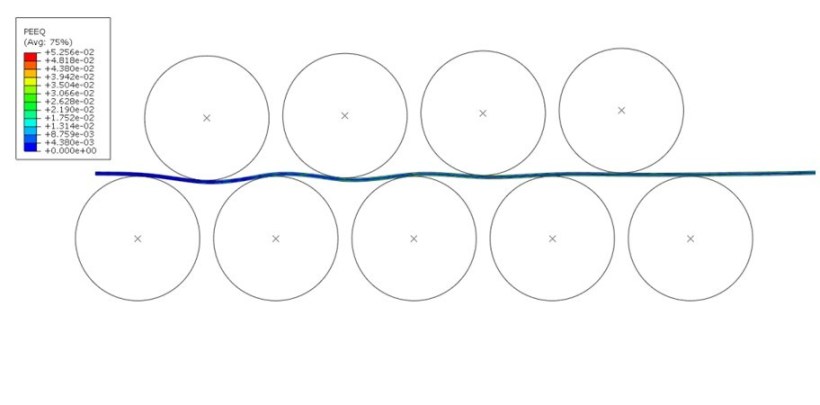

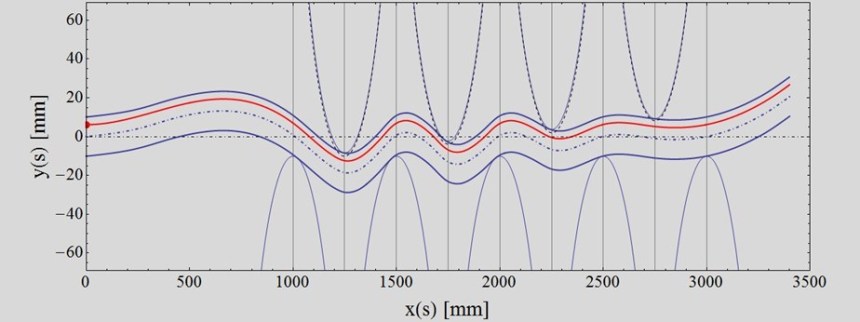

leveling maschine, credits: Voest AlpineThis picture shows the plastic-equivalent strain of a plate inside the leveler, credits: MathConsult GmbH(y-axis is not enlarged), credits: MathConsult GmbH

On May 23, 2019, UnRisk presented their mathematical and computational PRIIPs results in a seminar organized by Finanzverlag. Other speakers included representatives of the Autrian Financial Market Authority (FMA).

The PRIIPs regulation leads to serious problems when interest rates become negative. For the Euribor1m, this was the case for the first time in Sept. 2014.

The images

show Euribor1m paths starting on Sept. 5 and on Sept. 8, 2014. Negative

interest rates on Sept. 8 lead to completely different distributions when

obeying the PRIIPs regulation.

In summer

2019, MathConsult will employ 3 talents from Austrian high Schools to work as

“Young Talents” interns. Two of them will analyse data in computational

finance, one will work on Adaptive Optics for Extremely Large Telescopes.

Every year in spring, the Austrian research funding organization (in German “FFG – Forschungsförderungs-gesellschaft” awards the best 20 “young talents” out of 1500 high school students who did an internship in various companies and scientific research institutions for four weeks during the summer before. Young talents internships allow high school students to experience research and development live. The aim is to encourage girls and boys to follow natural sciences, engineering and technology. Each internship is funded with 1,200 Euro.

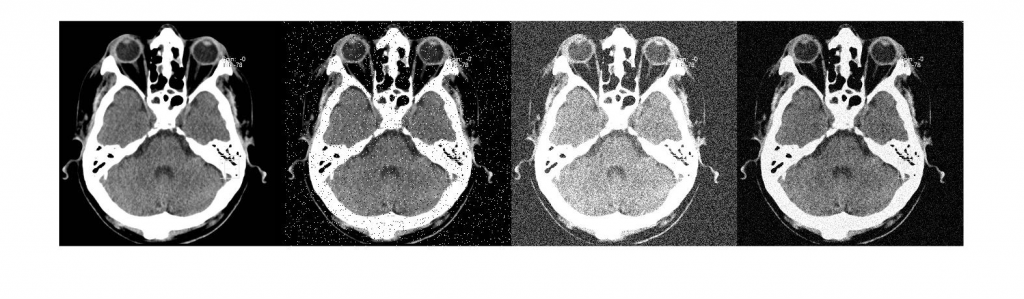

This is obviously one slice of a computer tomography scan of Andreas Binder’s nose sinuses (very left) + some artificial noise added (the other three images). Credits: MathConsult GmbH

Well, as mentioned above, only 20 students can win, now it’s my pleasure to proudly announce that Robert Niebsch is one of the lucky winners! He did his internship at MathConsult GmbH in Linz, Austria, a hosting company. The topic of Robert’s internship was “Medical image processing by diffusion filters”. Robert did a very good job. Congratulations!

The award ceremony took place on March 7, 2019 at Vienna’s Urania, where

all 2018 winners met and talked about their topics – and, finally they

found their way back home, accompanied by a new iPad mini and holding a

nice certificate in their hands.

Robert explaining what the skeleton is about. Credits: Astrid Knie The lucky talent with his – also very lucky (and proud) – supervisors Andreas Binder and Markus Pöttinger. Credits: Astrid Knie

Ann-Kristin

Baum (Radon Institute for Computational and Applied Mathematiocs, RICAM, of the

Austrian Academy of Sciences, presented results on Topological analysis of Functional

Mockup Units in liquid flow networks (joint work with Günter Offner and Michael

Kolmbauer).

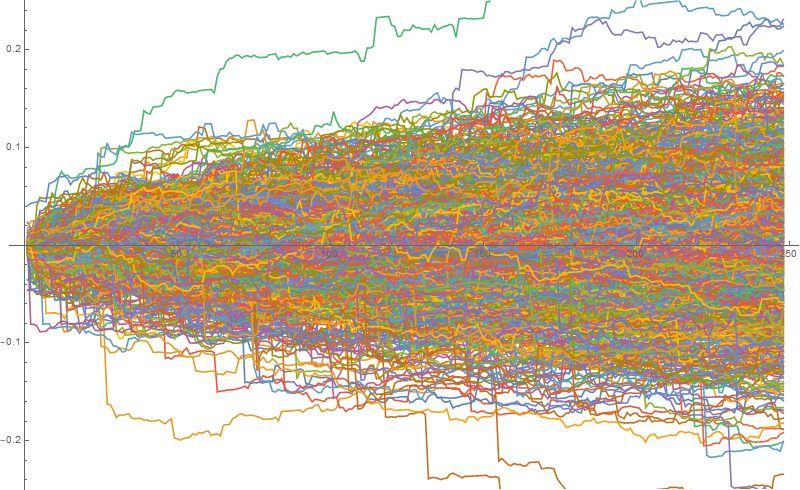

In the MathBox entry from 13 December, we showed the implied distribution of DAX returns when using the Cornish Fisher expansion.

As a rule

of thumb, this works nicely as long as the excess kurtosis is smaller than 8.

What happens if the implied distribution of returns is really fat-tailed?

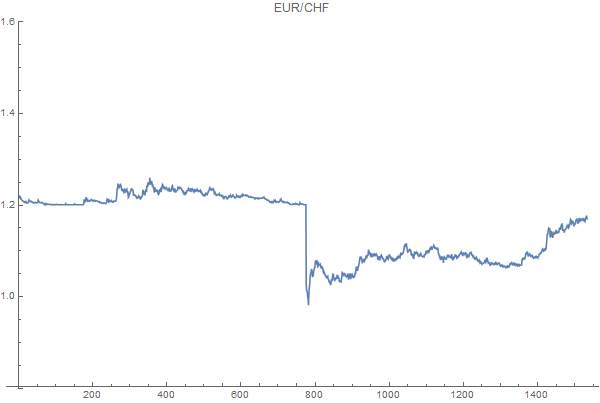

The

exchange rate of EUR and Swiss Franc between the years 2013 and 2017 showed an

excess kurtosis of 590. The Cornish-Fisher transformation between the implied

distribution of returns and the standard normal distribution is not bijective

any more and leads to weird distributions.

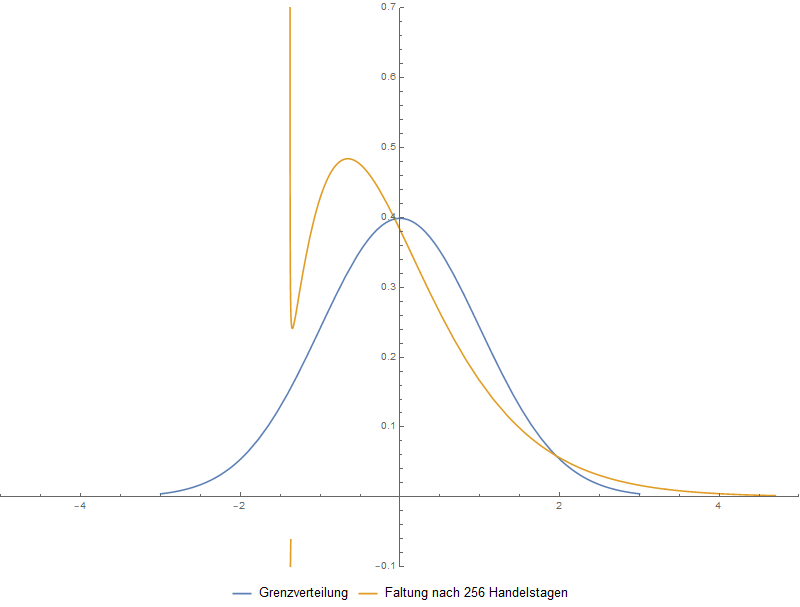

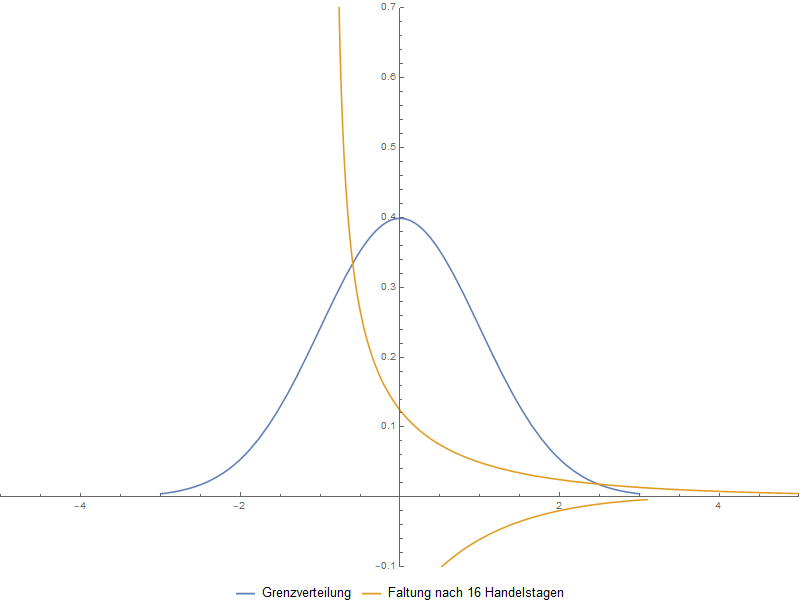

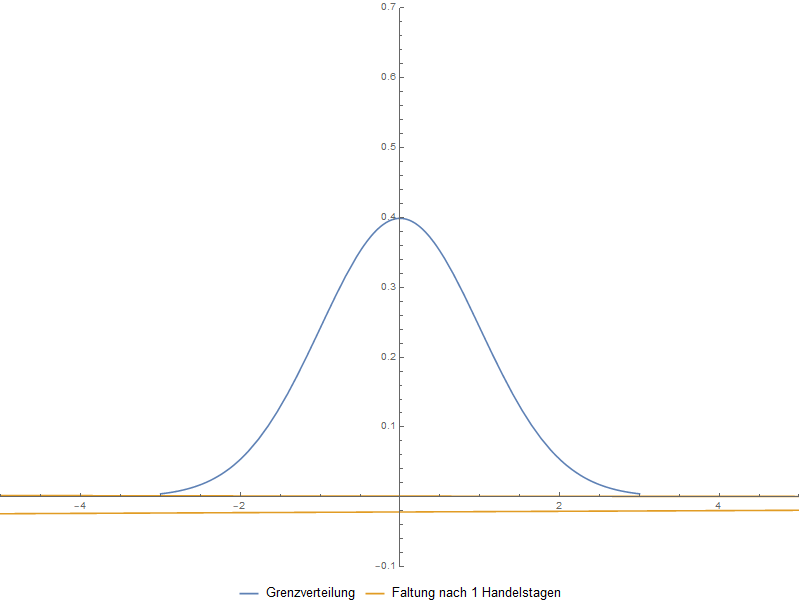

The plots show the implied “distribution” density (that is not a density) for the CHF EUR exchange rate return for a time horizon of 1, 16, and 256 business days, respectively.

Applying the Cornish-Fisher formulae for extreme cases like CHFEUR leads to misleading results in the risk reward section of a PRIIPs KID.

On Dec. 13,

2018, Andreas Binder gave a guest lecture on PRIIPs at the Bergische

Universität Wuppertal “The Mathematics of PRIIPs”.

Andreas Binder

With the

European Regulation 1286/2014 and the Commission Delegated Regulation 2017/653,

manufacturers of packaged retail and insurance-based investment products

(PRIIPs) are required to equip their PRIIPs with key information documents

(KIDs) describing the risk and the possible returns of these products on not more

than 3 pages.

For so

called category 2 instruments, the distribution of daily returns is based on

their means, variance, skewness and curtosis and a Cornish-Fisher expansion. By

doing so, fatter-tailed distributions are taken into account.

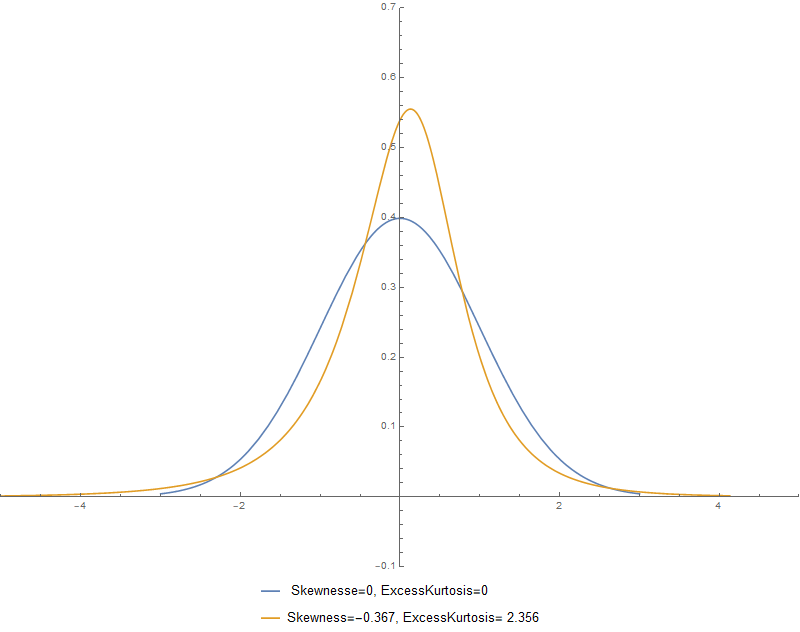

The plot shows the implied distribution derived form the Cornish-Fisher expansion for daily returns of the DAX between 2013 and 2017 (yellow line) compared to the normal distribution with the same variance (blue line). During this time period, Dax returns were left-skewed (skewness is negative) and fatter-tailed (excess kurtosis is positive).

MathConsult participates in the project “ROMSOC” within the Marie-Sklodowska-Curie action funded by the European Union. Onkar Jadhav, who joined us in Nov. 2018, will work on a European Industrial Doctorate on Reduced Order Models for Financial Risk Analysis (subproject Nr. 6 of ROMSOC, joint project between TU Berlin and MathConsult).

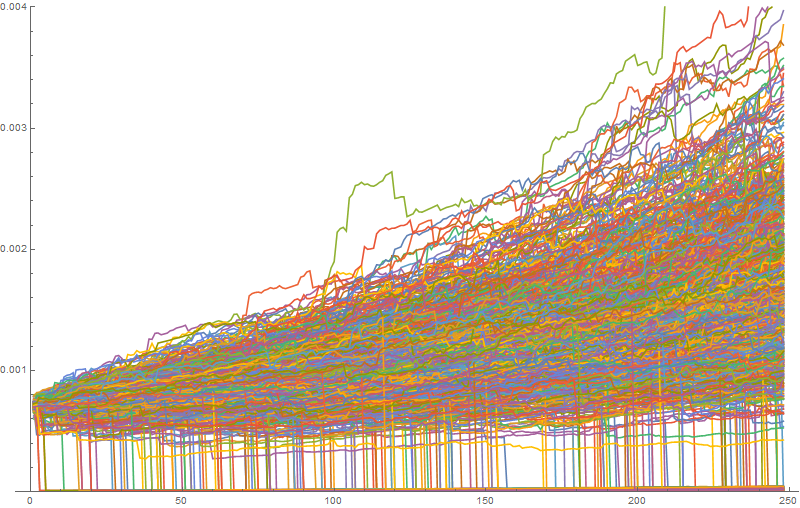

In the risk

analysis of financial instruments (or portfolios of them), one key task is to

calculate future returns and the possible risk under a wide range of scenarios.

In extreme cases, this may require the calculation of millions of scenarios,

calibrate financial models from these scenarios, and solve a stochastic or

partial differential equation for each of the calibrated models.

Developing reduced order models is a key technology in obtaining competitive solutions.

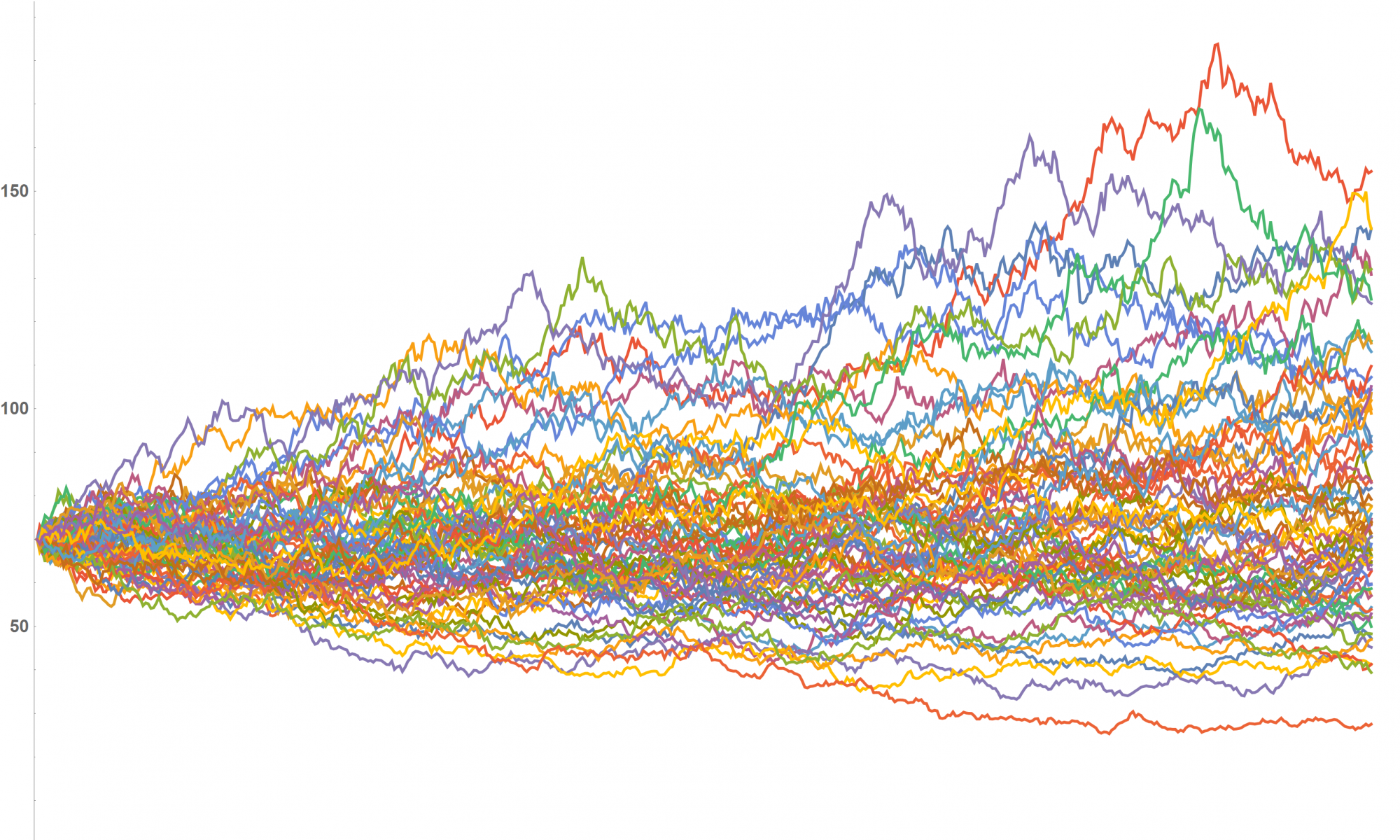

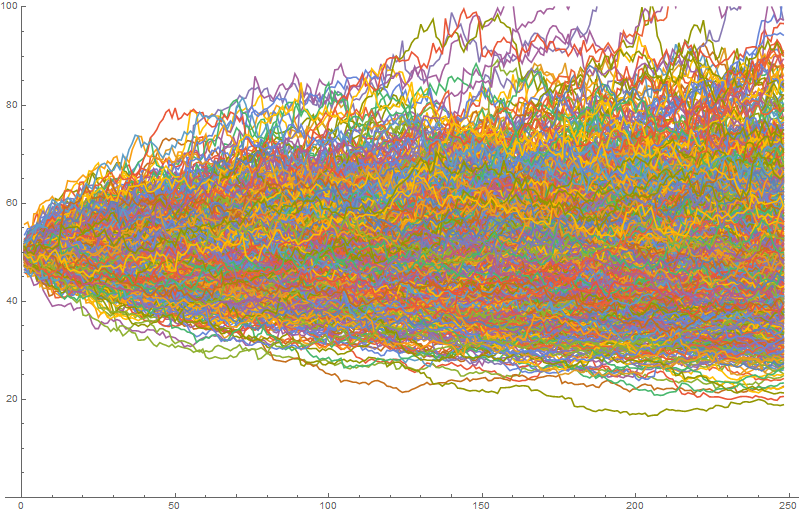

The image shows 1000 Monte Carlo paths (in the physical measure) with a time horizon of 1 year for a stock price.

Diese Website benutzt Cookies. Wenn du die Website weiter nutzt, gehen wir von deinem Einverständnis aus.