UnRisk Software Solutions for the Financial Industries

Financial institutions (banks, asset management firms, insurance companies) must valuate their assets and liabilities to analyse their financial risk on a regular (often: daily) basis. MathConsult have been developing their UnRisk® product family to achieve these tasks.

Valuation

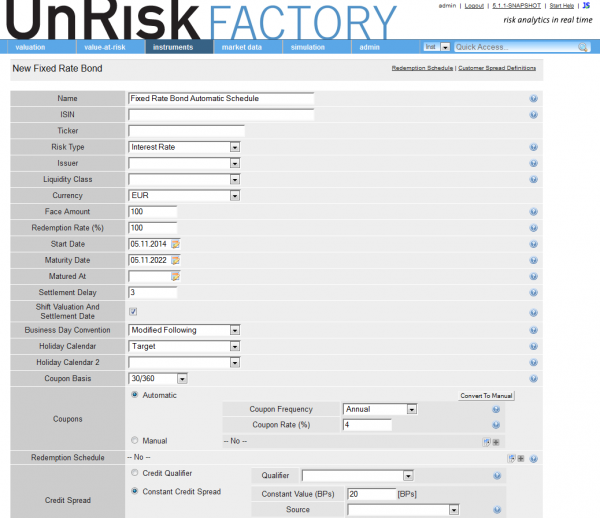

Depending on the specific details of financial instruments, valuation (meaning the calculation of a fair value) may be fairly easy, e.g., by looking up exchange traded equity prices or by discounting the cashflows of a fixed rate bond. Over the counter (OTC) instruments, on the other hand, are often quite complex and require the solution of a stochastic or a partial differential equation, equipped with appropriate terminal, interface and boundary conditions.

MathConsult has been working on a wide variety of valuation problems since 1997. The UnRisk ENGINE, which was (in its first version) released in 2002, covers now a wide range of financial instruments from various asset classes, and allows to apply different financial models for the valuation tasks needed.

Workflow in valuation and risk analysis

The typical workflow for the valuation of a structured financial instrument is the following:

- Choose a model for the stochastic movement of the underlying. In the case of fixed income instruments, an interest rate model (e.g., Black76, Bachelier, Hull-White, Black-Karasinski, Libor market model) is chosen.

- Calibrate the parameters of the model by robust parameter identification techniques using market data of liquidly traded basic instruments.

- Apply the appropriate forward valuation routines for the structured instrument. In UnRisk, Green’s functions, finite element techniques, (Quasi)Monte Carlo simulation, and Fourier techniques are implemented.

Risk management and UnRisk FACTORY automation.